Hong Kong dragged deeper into recession by Covid-19 pandemic – business live

Hong Kong’s lurch deeper into recession hasn’t brightened the mood in the markets.

The main European indices are all sharply lower still, as investors worry about the escalating tensions between the US and China – and the threat of a new trade war.

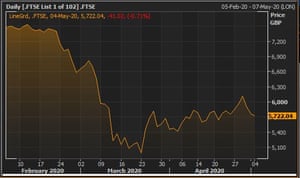

Britain’s FTSE 100 has recovered some ground, but that’s partly because the pound has dropped against the US dollar (down almost one cent to $1.242). That boosts multinationals.

The FTSE 250, which is more focused on the UK, is down 1.3%.

[Reminder: European markets missed out on Friday’s sell-off because they were closed for May Day].

Back in the UK, sugar and starch producer Tate & Lyle has reported that sales were affected by the Covid-19 lock down.

Sales of Tate & Lyle’s bulk sweeteners slumped by 26% in April, due to bars, cinemas, restaurants and sporting venues all shutting down.

Volumes of the rather-unappetising sounding “industrial starch” fell 9% — due to “reduced demand for paper and packaging following the closure of schools, offices and a general decline in economic activity”.

But sales of ‘food and beverage’ products to consumers jumped 18% as people stocked up on staples (such as golden syrup and granulated sugar).

Tate & Lyle says:

Earlier in the month, demand was strong for ingredients used in packaged and shelf-stable foods as consumers in North America and Europe filled their pantries for consumption at home.

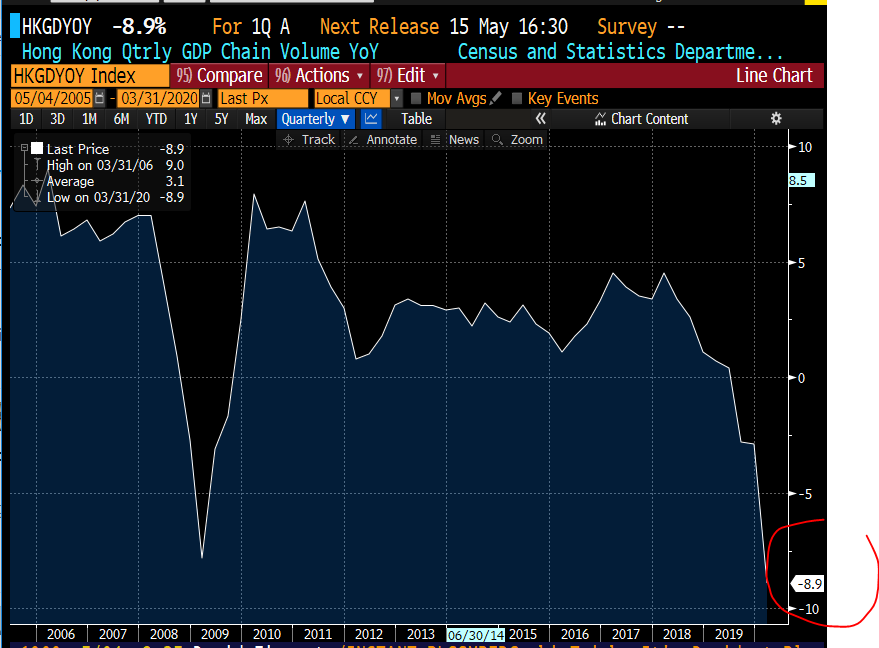

Newsflash: Hong Kong’s recession has deepened as the Covid-19 pandemic hits its economy.

Hong Kong’s GDP shrank by 5.3% in the first quarter of 2020, official figures show. That’s a very sharp contraction, extending its economic downturn.

On an annual basis, the City state’s economy is now 8.9% smaller than a year ago – due to coronavirus shutdowns, last year’s pro-democracy protests, and the US-China trade war (which may be flaring up again…)

Trinh Nguyen

(@Trinhnomics)The big dip 📉📉

Hong Kong GDP-8.9%YoY (don’t forget it was the only economy in contraction in 2019 in Asia) pic.twitter.com/wN9wqq4kzD

David Ingles

(@DavidInglesTV)Hong Kong registers record economic contraction in 1Q and the sixth quarterly contraction in the last eight quarters. Gaaaaaaaa pic.twitter.com/gyRTH0IB5j

David Ingles

(@DavidInglesTV)Hong Kong GDP… oh man.

In a statement, Hong Kong’s government said the pandemic had caused a “severe contraction” in global economy activity. It now fears the economy will shrink by 7% this year, and predicted that exports will remain under “notable pressure” in the near term.

Yolande Chee

(@YolandeChee)Hong Kong Q1 GDP much weaker than expected at -8.9% y/y. Third consecutive quarter of negative growth. Government revises 2020 forecast to -4% to -7%. Says local economic activity will remain subdued in the near term if the threat of pandemic continues.

France, Germany and the Netherland’s manufacturing sectors also slumped last month, according to Markit’s new survey of purchasing managers.

They confirm the message from the ‘flash’ PMIs two weeks ago – activity contracted in April even faster than after the financial crisis:

IHS Markit PMI™

(@IHSMarkitPMI)🇩🇪 Germany #PMI data for April emulates that seen for lockdown countries, with output levels collapsing at an even quicker rate than during financial crisis. Read more at t.co/cawrdpv5CL pic.twitter.com/DIPtpAWHWX

LiveSquawk

(@LiveSquawk)French Markit Manufacturing PMI – April Report #PMI t.co/ketE1MrGRQ pic.twitter.com/3C8CXFecO8

IHS Markit PMI™

(@IHSMarkitPMI)Dutch manufacturing output contracted at a survey record rate in April amid the #COVID-19 pandemic, with the PMI down to a near 11-year low of 41.3 in April (50.5 – March). New business also declined at the quickest pace on record. More here: t.co/hdm5PrnSU9 pic.twitter.com/yICez6lSfa

This has dragged the final Eurozone Manufacturing PMI down to 33.4, slightly worse than the flash reading of 33.6– showing an extremely steep contraction (a reading of 50 would show activity was flat).

European stock markets have opened in the red, as traders respond to the latest US criticism of China.

The Europe-wide Stoxx 600 index has dropped by 2.6%, with France’s CAC and Germany’s DAX both shedding 3%.

Investors are scrambling to sell stocks having been on holiday last Friday (when the threat of a new US-China trade war emerged).

In London, the FTSE 100 has dipped by 40 points, or 0.7%, to 5722. That’s an eight-day low, meaning last week’s brisk rally has been wiped out.

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Investors are jittery today after the White House intensified its criticism of China over the Covid-19 pandemic, fuelling fears of a new breakdown in relations between the two powers.

Overnight, Donald Trump repeated his claim that the virus emerged from the Wuhan Institute of Virology (something previously denied by China) and that Beijing couldn’t “put out the fire”.

He told Fox News:

“I think they made a horrible mistake and they didn’t want to admit it…

“My opinion is they made a mistake. They tried to cover it, they tried to put it out. It’s like a fire.

Trump also suggested that new tariffs on China could be the ‘ultimate punishment for Beijing, as a penalty for bungling the coronavirus outbreak.

RANsquawk

(@RANsquawk)– US President Trump said tariffs would be the ultimate punishment on China and warned that that if China doesn’t buy US goods, the US will end the trade deal

Hours earlier, US secretary of state, Mike Pompeo, said there was “enormous evidence” the coronavirus outbreak originated in the laboratory — without providing the proof to back up the claim.

China seems likely to be a key issue in the US presidential election – especially as the president can’t boast about the soaring stock market or the strongest economy in history.

Stephen Innes, chief global markets strategist at AxiCorp, writes:

The US media is pointing to the growing possibility that China will be the focal point of the 2020 election campaign. Polls conducted by President Trump’s campaign suggest that China will be an ongoing issue, according to Republican sources cited by Politico.

The Democrats are examining a harder line on China to boost their chances. Either way, China will be in the US spotlight and not in a pleasant way.

Fears of a new US-China trade war are overshadowing hopes that the global economy could tiptoe its way towards more normal conditions in the coming weeks.

Britain’s FTSE 100 is expected to drop by 40 points, or over 0.5%, adding to Thursday and Friday’s losses. There will be deeper sharper losses in continental Europe, where traders are playing catch-up after Friday’s May Day holidays.

David Buik

(@truemagic68)Though Beijing & Tokyo are closed today, investors realise “The world has an economic problem to face” plus Sino/US jingoistic rhetoric to consider- Suggested European opening calls – FTSE 100 -32 at 5723, DAX -115 at 10491, CAC 40 -36 at 4536, DJIA futures -175 at 23555

Most countries have continues to report a slowdown in new cases and deaths from Covid-19 – with the global death toll now standing at over 247,000. Italy is starting to lift its lockdown today, but there is public disappointment and anger that travel is still restricted and some shops aren’t allowed to open.

The agenda

- 9am BST: Eurozone manufacturing PMI for April: likely to confirm the worst downturn on record

- 9.30am BST: Hong Kong GDP for Q1 2020: likely to show another contraction

- 3pm BST: US factory orders: expected to fall around 10%

Read the original article at The Guardian