UK economy in ‘unprecedented downturn’ as activity keeps falling – business live

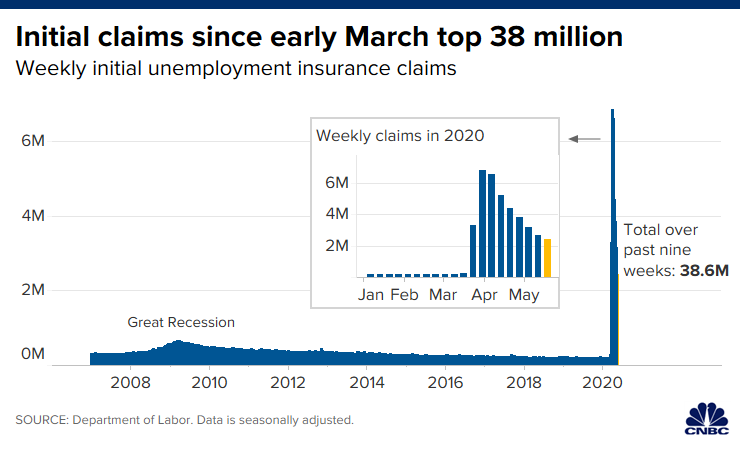

America has just passed a grim milestone in its unemployment crisis.

Glassdoor senior economist Daniel Zhao has spotted that more jobs have been lost in the last nine weeks than during the last recession a decade ago:

“Today’s sky-high unemployment insurance claims report brings the total UI claims to 38.6 million and surpasses yet another historical benchmark. In only nine weeks, unemployment claims made during the coronavirus crisis have already exceeded the 37 million claims made over the entire 18 months of the Great Recession.

The coronavirus crisis continues to inflict swift and deep impacts on the labor market at a near unprecedented clip.

Before Covid-19, the idea of more than two million Americans losing their jobs in a single week would be unimaginable, let alone 38 million joining the unemployment ranks in two months.

As this tweet shows, the job losses since March absolutely dwarf the impact of the financial crisis – wiping out all the gains since then.

Newsflash: Another 2.4 million Americans filed new claims for unemployment benefit last week, as the US jobs crisis deepens.

That’s down from 2.6 million in the previous seven days (which has been revised down from 2.9m).

But it’s the ninth week in a row in which millions of US citizens signed on for welfare benefits, having lost their job in the lockdown.

The total number of initial claims filed since mid-March is now over 38 million, or over a fifth of the US labor force.

Equitable Growth (@equitablegrowth)

2.4 million workers applied for #unemploymentbenefits in the week of May 10–16 according to the @USDOL’s Weekly Unemployment Insurance claims report released today. Since the onset of the #coronavirus crisis in mid-March, 38.6 million workers have filed initial UI claims. (1/4) pic.twitter.com/vHkaotVorh

The number of continued claims (for workers who were already on the jobless total) also jumped again to over 25m, from 22.5m.

Joseph Brusuelas (@joebrusuelas)

US Initial Claims: Continuing claims for the week ending May 9, which will inform the official, estimate of the May unemployment report, increased to 25 million, resulting in an insured unemployment rate of 17.2%.

Oof! US department store Macy’s has warned that its sales have fallen by around 45% in the last quarter, as the coronavirus shutdown drove it into the red.

Preliminary results show that sales at Macy’s in February-April fell to between $3,000m and $3,030m, down from $5,504. It made an operating loss of around $1.1bn, down from an operating profit of $203m a year earlier.

The company shut all its stores – including department chain Bloomingdale’s and beauty chain Bluemercury – on 18 March, leading to a slump in takings.

“This is a challenging time for the country, for retail and for Macy’s, Inc. COVID-19 has impacted the lives of many of our colleagues and customers, and health and safety remain our top priority. We closed all of our stores – Macy’s, Bloomingdale’s and Bluemercury – on March 18, which had a significant impact on our first quarter results,” said

Jeff Gennette, chairman and chief executive officer, said it is a challenging time for the country, for retail and for Macy’s itself.

“Looking back, our performance in February was solid and in line with our expectations, but we saw a precipitous decline in sales with the stores closure in March. As a developed omnichannel retailer, we experienced a steady uptick in our digital business in April, which was encouraging, but only partially offset the loss of sales from the stores.

The digital performance was driven by strong execution and enhanced fulfillment options, including curbside pickup where allowed.”

Lauren Thomas (@laurenthomas)

JUST IN: Macy’s forecasts a first-quarter loss of up to $1.1 billion, compared with net income of $203 million a year ago. “With two weeks of results from reopened stores, customer demand is moderately higher than we anticipated,” CEO says. $Mt.co/mPL3flRhnc

Wall Street is expected to open lower, with the Dow down 145 points (roughly 0.6%) in pre-market trading and traders nudging the safe-haven dollar a little higher.

Kathy Jones (@KathyJones)

Thursday: risk off tone with stocks down, dollar firm and bond yields edging lower. PMIs still in deeply negative territory.

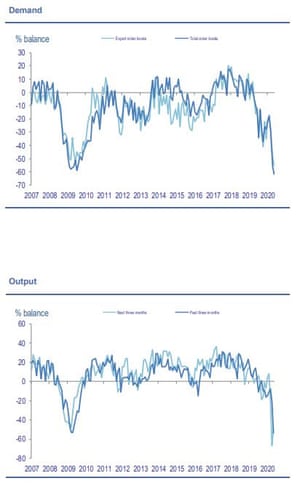

Newsflash: UK manufacturing output has fallen over the last quarter at the fastest rate since at least 1975.

Output volumes fell in 15 of 17 manufacturing sub-sectors in March-May, according to the latest healthcheck from the CBI.

Motor vehicles and transport equipment, and food, drink and tobacco, suffered the sharpest tumbles. while pharmaceuticals and electronic engineering output rose.

This pulled down the CBI’s measure of output volumes in the last quarter to -54%, from -21% in April (the balance between firms reporting higher output vs lower).

This isn’t a massive surprise, given the widespread shutdowns across UK factories to fight the Covid-19 pandemic.

But worryingly, manufacturers predict that output volumes will keep falling over the next three months, with many reporting that their order books have shrunk alarmingly.

The survey also found that:

84% of respondents had seen a negative impact on their domestic output.

68% of manufacturers reported a negative impact on their international output.

51% of manufacturers reported a partial shutdown/closure.

59% of manufacturers mentioned that they had temporarily laid off staff, while 9% reported permanent layoffs.

74% of firms had faced cash flow difficulties.

Anna Leach, CBI deputy chief economist, says UK manufacturing faces a “challenging” future:

“These results show that UK manufacturers are still grappling with the impact of the pandemic.

Production levels have fallen even more sharply as firms experience collapsing demand and supply chain disruption, leading some to temporarily shut down their factories. The sector is bracing for what will be a challenging period.

The CBI’s manufacturing survey to May 2020 Photograph: CBI

Duncan Brock, Group Director at CIPS, fears that a second wave of Covid-19 infections could undermine hopes of a recovery (sending the PMI skittering back down to April’s record lows).

“This month saw another steep fall in overall business activity, surpassing for the third time the rates of decline seen during the global financial crisis in 2009. No new orders, premises shut down and furloughed staff unable to return to work were at the heart of the desolation as business struggled to continue with two hands tied behind their back.

Even some heavy discounting by companies did little to offset their losses which are likely to be just the tip of the iceberg with businesses failing in increasing numbers. “As the sectors prepare for a further easing in restrictions and becoming covid-ready for staff to return, the danger on the horizon is a second wave of infections threatening the health of the nation and dampening consumer confidence still further.

In addition, if this intensity of job cuts continues, purse strings will be drawn tightly shut and spending severely curtailed, putting further pressure on the UK economy and ensuring any recovery is many years into the future.”

Here’s Andrew Wishart of Capital Economics on today’s UK purchasing managers survey:

Taken literally the fact the flash composite PMI remained well below the no-change level of 50 in May suggests that activity fell further as it should compare activity to the previous month. But many respondents appear to be answering the alternate question of “how is activity compared to normal?”. So instead it appears to be suggesting that the low point for activity was reached in April, but that it is still well below normal in May.

The recovery in the manufacturing PMI from 32.6 to 40.6 is probably a sign that some industrial plants have reopened on government advice. And the services index recovered from 13.4 to 27.8, in line with anecdotal evidence that firms have restarted limited operations, such as take-out options from restaurants.

IHS Markit PMI™ (@IHSMarkitPMI)

🇬🇧 Flash UK Composite #PMI at 28.9 in May (13.8 – Apr) to signal further contraction in the UK economy, but with rates of decline softening from April as COVID-19 restrictions were eased. Read more: t.co/zGCpgQst0kpic.twitter.com/CSWpXZO47F

A few weeks ago, there was lots of talk about V-shaped recoveries.

Economists hoped that growth would bounce back sharply from the initial shock of Covid-19, as companies rapidly caught up on lost business.

It always seemed a little optimistic — no-one is going to get two haircuts, order three restaurant specials or watch four football matches in a day once the crisis is over (but lets not rule out two specials….)

The message from today’s PMI surveys is clear — businesses across the eurozone and UK have suffered major damage under the lockdown, and the downturn is not over.

Neil Birrell, Chief Investment Officer at Premier Miton, says the recovery is some way away:

“The PMI data in from the UK and Europe suggests that the outlook is improving. That is to be expected, as the surveys are taken mid-month and economies were more open than they were in mid-April. But with UK Composite PMI at 28.9, albeit up from 13.8 in April, and the Eurozone Composite PMI reading at 30.5 the outlook is still grim. Markets may well take this as a sign that the nadir has been reached, although recovery is some time off.”

James Smith and Bert Colijn of ING agree that the recovery certainly won’t resemble a perky V.

James Smith (@SmithEconomics)

Weak #PMI readings echo Google’s Mobility data that show #UK activity still significantly down on pre-virus levels. More evidence that a ‘V-shape’ recovery now very unlikely pic.twitter.com/ciZGiJgmg9