UK retailers pessimistic as economy reopens; Covid-19 worries markets – as it happened

And finally, the London stock market has ended the day with small gains – after a choppy days trading.

The FTSE 100 has closed 23 points higher at 6147 points, a gain of 0.4%. That’s a small rebound after yesterday’s 3% slide.

Despite this morning’s gloomy CBI survey, retail chain JD Sports was the top riser on the FTSE 100, up 3.8%.

Investment group Standard Life Aberdeen (+3.7%) and private equity group 3i (+3.6%) also rallied, following the jump in financial stocks after regulators relaxed regulations on US banks.

Top fallers included Rightmove, catering company Compass and hotel group Whitbread – all vulnerable to any second wave of Covid in the UK.

The worse-than-expected US jobless data didn’t cause much alarm in the City, with traders mainly focused on the latest Covid-10 developments. Larry Kudlow’s insistence that America won’t have another lockdown may have calmed nerves, however that pledge could be tested if Covid-19 cases keep rising.

Thee latest warning from the iMF about stock market bubbles should also encourage investors to wonder if the recent rally has gone too far….

On that cheery note, goodnight! GW

Photograph: Dado Ruvić/Reuters

Disney has moved to axe its kids TV channels in the UK after more than two decades on air and move them to its Disney+ streaming service.

Disney, which launched the £5.99 streaming service in the UK on the 24th March as the nation went into lockdown due to the coronavirus, has taken the decision after failing to reach a new commercial agreement to continue to air the channels on Sky, BT and Virgin Media.

A spokesman for the company said:

“From 1 October, Disney+ will become the exclusive home for content from Disney Channel, DisneyXD and Disney Junior in the UK.”

Disney+ has grown rapidly globally to more than 54m subscribers, although many are on one-year free deals, and is estimated to have almost two million subscribers in the UK, according to Ampere Analysis.

Disney+ already offers the kids channels, however the content is older while Sky, BT and Virgin Media have traditionally aired the newest series of shows such as Mickey Mouse Club.

The failure to reach a commercial deal, and Disney’s ability to now turn to its own service as an alternate route to consumers, shows the rising threat which streaming services pose to traditional TV operators.

Disney still has a range of licensing deals in place with Sky, including for hit show The Simpsons and its blockbuster movie franchises, which could ultimately come under threat in a similar way in the future.

Netflix is the biggest streaming service in the UK with 12m subscribers, followed by Amazon’s Prime Video, with 10m. Sky’s Now TV has about 1.6m subscribers.

Shares in US banks have jumped, after banking regulators unveiled a pair of rules that will make life easier for large banks with complex trading and investment portfolios.

Reuters has the details:

One rule wraps up a long-running effort by Republicans to overhaul the so-called “Volcker Rule,” clearing the way for banks to make larger investments in riskier funds like venture capital funds.

The second relieves banks from having to set aside cash to safeguard derivatives trades between affiliates within the same firm. The move hands a win to big global banks that had lobbied for the relief, as industry estimates it could free up as much as $40 billion in previously reserved cash.

Goldman Sachs has now jumped to the top of the Dow leaderboard, up 2.6%, followed by JP Morgan (up 2.1%). This has lifted the Dow into positive territory, after its earlier slide.

One of Donald Trump’s top advisors has insisted that the US economy won’t lock down again, even if Covid-19 cases keep rising.

Larry Kudlow, director of the United States National Economic Council, told Fox Business that there may be individual “spikes and hot spots” in certain places, but not another national shutdown.

Monica Alba (@albamonica)

NEC Chair Larry Kudlow maintains the White House doesn’t see a second wave of coronavirus coming. Asked if they’re concerned about highest daily total of new cases, he said: “We’re gonna have hotspots, no question” but “we just have to live with that” and “we will not shut down”

June 25, 2020

Chinese company Huawei’s UK offices in Reading, west of London. Photograph: Daniel Leal-Olivas/AFP via Getty Images

Huawei has said it will spend £1bn on a new chip research and development centre outside Cambridge, after receiving planning permission from the local council.

The move to build the facility, which will create 400 local jobs, comes as the government considers reducing the controversial Chinese technology company’s involvement in the rollout of the UK’s 5G mobile networks to zero. In January, the government said that Huawei could be involved in building the UK’s 5G networks, but with a 35% cap on the use of its equipment.

Last month, the UK’s National Cyber Security Centre, a branch of GCHQ, launched an emergency review into the use of Huawei equipment after the US put more export controls on the Chinese company.

Huawei insisted that the new 500 acre campus, which was approved by the South Cambridge District Council by nine votes to one on Thursday, was not a political play to curry support.

Victor Zhang, vice president at Huawei, said:

“It has been suggested that our £1bn investment has been timed to coincide with the debate over Huawei’s future in the UK’s 5G infrastructure.

In January the government said Huawei can continue to work with customers on 5G in the UK. The Cambridge investment began more than three years ago in 2017, well before the subject of Huawei and 5G was raised in the UK. Huawei did not pick the timing of the approval… by South Cambridge council.”

The new site, which will be about 15 minutes from chip designer ARM, will be used to develop and manufacture semiconductor technology, called optoelectronics, aimed at speeding up data transmission over fibre broadband networks.

Huawei, which employees 1,600 people in the UK, bought the 550-acre site for £37.5m in 2018.

The International Monetary Fund has warned that the recent stock market rally may have run too far – and is vulnerable to a correction.

In its latest global financial stability report, the IMF said the surge in stocks since late March suggested an optimism that was not matched by the economic data.

“Markets appear to be expecting a quick ‘V-shaped’ rebound in activity.

“This has created a divergence between the pricing of risk in financial markets and economic prospects.”

The IMF is also concerned that the rally appears to be fuelled by central bank stimulus schemes – raising the risk of a crash if the punchbowl is taken away.

After 20 minutes, the Dow Jones industrial average is now down 199 points, or 0.8%, at 25,245.

That’s its lowest level since Monday 15 June, leaving the index flat for the month and 11% down this year.

Industrial stocks, basic materials makers and consumer goods firms are leading the sell-off. Boeing is down 2.5%, on fears that a surge in Covid-19 cases will cause further damage to the travel sector.

This is the 14th week in a row in which new US jobless claims exceed one million – a previously unprecedented level (and indeed scarcely believable before the lockdown).

Glassdoor senior economist Daniel Zhao says the US jobs market remains fragile.

The labor market continues its lethargic recovery as we see another week of only modest declines in the tens of millions of Americans continuing to claim UI benefits amid an ongoing pandemic. While recent economic indicators like the May jobs report stoked optimism for a swift recovery earlier this month, the slow improvement in continuing claims puts a damper on those high hopes.

Looking ahead to the June jobs report next week, we’re likely to see more signs of a labor market only modestly improving, balancing precariously between a speedy V-shaped and a much slower recovery.”

Zhao also points out that PUA claims – paid to gig economy workers who are sidelined – are also rising.

Daniel Zhao (@DanielBZhao)

2. Continuing UI claims have fallen, but continuing PUA claims have risen by more.

Overall continuing claims (inc other programs not shown in the chart) increased to 29M for week ending Jun 6.

This data is on a longer lag, but further evidence of a slower/stalling recovery. pic.twitter.com/aNu5br3TcP

June 25, 2020

Some snap reaction to the latest US jobless figures:

Randy Frederick (@RandyAFrederick)

At 1.480M, Initial Jobless Claims came in above the 1.320M estimate, and just below last week’s 1.540M level; this was the 12th weekly decline. Claims peaked on 3/28 but remain VERY high. t.co/maIeV4Rfa2pic.twitter.com/kDdvZabgho

UI claims continue to slowly recede but levels still recessionary. We’re entering the start/stop, slog part of the crisis. We’ll get some good and bad numbers, trends will mostly be in the right direction, but as long as virus control is so badly managed from the top… pic.twitter.com/N18o6Mn5FF

June 25, 2020

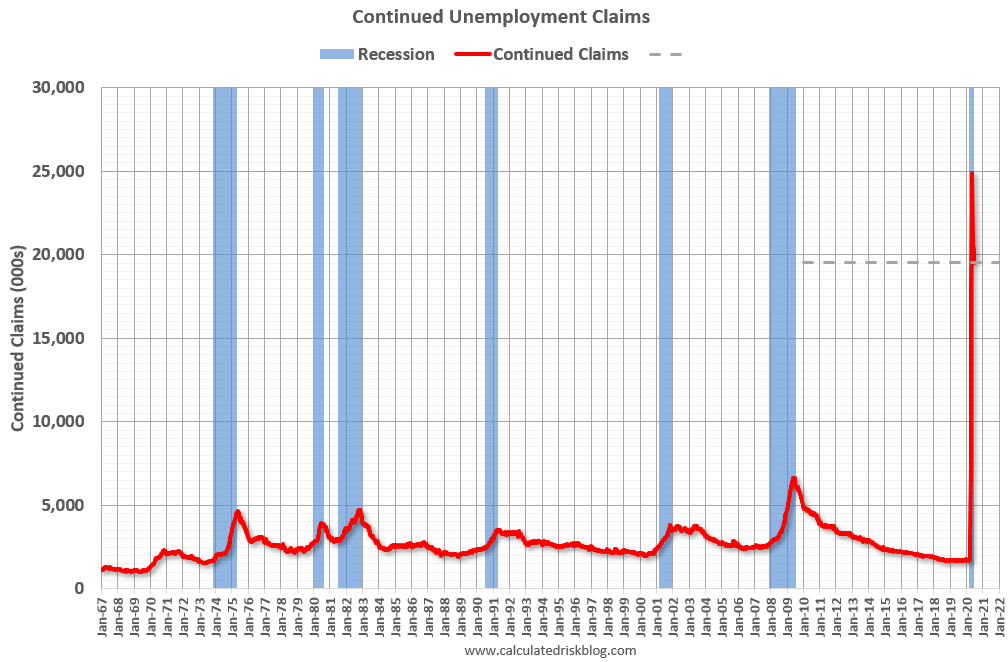

Slightly more encouragingly, the number of Americans who have been claiming unemployment benefit for at least a fortnight has dropped.

This ‘continued claims’ total has dropped from 20.289m to 19.522m – still alarmingly high.

Steven Rattner (@SteveRattner)

Continuing jobless claims fell below 20M for the first time since mid-April, suggesting that more workers being reabsorbed into the labor force. Still a long way to go. pic.twitter.com/H8zkcxHa3z

June 25, 2020

Newsflash: Nearly 1.5 million Americans filed new claims for unemployment benefit last week.

That’s worse than expected — economists had expected 1.3m fresh job losses. It’s barely lower than the previous week, when 1.54m initial jobless claims were filed.

This suggests America’s economy is struggling to emerge from its slump, and that some companies are still laying staff off.

It also means that at least a million Americans have lost their jobs every week since mid-March, when the initial jobless claims smashed the previous record of under 700k.

Jason Brooks (@brookskcbsradio)

#Jobless claims continue to mount with another 1.48 million first time claims, down just slightly from the prior week. That’s around 48-million initial claims over the past fourteen weeks. And #Macy’s is adding to the long line announcing its cutting 3900 corporate jobs

June 25, 2020

US department store Macy’s has just announced it is cutting 3,900 corporate jobs.

The move will save around $364m, Macy’s says, as it tries to cut costs to ride out the coronavirus pandemic.

Another blow to America’s labor market, just minutes before we get the latest weekly jobless data….

CNBC (@CNBC)

Macy’s to slash 3,900 corporate jobs in restructuring t.co/uXLyFT7oU1

June 25, 2020

UK retailers are right to be concerned about their sales prospects, says Howard Archer of the EY Item Club.

He suspects demand for big-ticket items will remain weak, especially among workers who are currently furloughed….

While there may well be a significant initial element of ‘pent-up’ demand for some retailers following their re-opening, further out the upside for may well be capped by cautious consumers.

Consumer spending has clearly taken a substantial downturn as a result of COVID-19and is likely to remain under pressure for the near term, at least. Many people have lost their jobs, despite the supportive government measures. while others may be worried about job security once the furlough scheme ends in October.