Markets slide as EC predicts deeper eurozone recession – as it happened

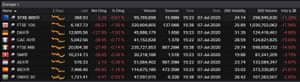

And finally… Britain’s FTSE 100 has ended the day down 1.5% or 96 points at 6189 points.

Hotels group Whitbread led the fallers, down 5.5% after it warned of subdued demand at City locations (although regional sites are more popular).

Packaging firm Smurfit Kappa (-4.1%), conference organiser Informa (-4%) and property company Land Securities (-3.7%) were also among the fallers, as investors worried that hopes of a V-shaped recovery from the pandemic were too bullish.

With Europe facing a deeper recession than feared, and UK house prices dipping again, there’s plenty of reasons to fret. But the surge in China’s stock market in recent days, to five-year highs, could suggest that markets have further to climb…..

On that note, goodnight! GW

Shares in fast fashion brand Boohoo have sunk for the second day, as several customers dropped its clothes over conditions at its Leicester suppliers.

Boohoo shares closed nearly 12% lower tonight, knocking around £440m off its value – on top of the £1.1b shed on Monday.

Asos, Next, very.co.uk and Zalando have all distanced themselves,after claims that people making Boohoo clothes weren’t protected from Covid-19, and were paid less than the minimum wage.

My colleague Archie Bland explains:

Next said its approach was “based on trust” but that the allegations could not be ignored, and had launched its own investigation. It said it was “not pre-judging the outcome of this process and no final decision has been made” but that the items would be suspended in the meantime.

Zalando, a Berlin-based online retailer which had €6.4bn sales in 2019, joined Next and Asos in dropping Boohoo, and all references to the company had been removed from their websites.

Archie Bland (@archiebland)

So that’s four e-tailers which have now dropped Boohoo. Surely more to follow. While it accounts for mid-single digits of total sales, it’s a PR nightmare, and makes influencer exodus more likely. And millions more off the share price today.

July 7, 2020

More here:

The gold price has hit a new eight year high, touching $1,796 per ounce for the first time since 2012.

Gold appears to be being driven higher by several factors, including record low interest rates and the expansive central bank money-printing operations.

Investors are also keeping an eye on Brazil, where president Jair Bolsonaro was tested for coronavirus and had his lungs scanned, after reportedly showing symptoms associated with Covid-19.

French news magazine Valeurs Actuelles reported this afternoon that Bolsonaro has tested positive – and that’s just been confirmed by the man himself.

VirginieJacobergerL (@VJacobergerL)

Exclusif, prsdt Jair #Bolsonaro tested positive for #covid19 , last story published at 1 pm (Paris time), the result was confirmed to @Valeurs by 2 sources / gvt #Brazil t.co/7VCV3F4fNu

July 7, 2020

Valeurs actuelles ن (@Valeurs)

🔴 Selon une source proche du gouvernement brésilien, le président Jair Bolsonaro a été confirmé positif au #coronavirus, rapporte @VJacobergerL ⤵️https://t.co/jR1KwmgA97

July 7, 2020

Today’s downbeat forecasts intensify pressure on EU leaders to agree a major Covid-19 recovery plan.

Our Brussels correspondent Jennifer Rankin explains:

The gloomy figures were published 10 days before EU leaders meet in Brussels to search for agreement on a €750bn (£678bn) recovery plan, following a landmark Franco-German proposal for grants to help the hardest-hit countries.

While all players say they want a deal in the summer, the plan continues to face fierce resistance from the self-styled “frugal four”, Austria, Denmark, Sweden and the Netherlands, which oppose grants, favouring loans.

The European commission argues that loans will add to national debt burdens, while fearing an uneven economic recovery could leave some countries stuck in the economic slow lane for years to come.

“The risk of an increasing divergence was the rationale for proposing our common recovery plan and this risk appears to be materialising,” said Paolo Gentiloni, the EU commissioner for the economy. “This is why it is so important to reach a swift agreement on the recovery plan proposed by the commission – to inject both new confidence and new financing into our economies at this critical time.”

European stock markets remain solidly in the red, with around 45 minutes trading to go.

Predictions of an even deeper eurozone recession this year, and a slower recovery, have dampened the mood – with that Melbourne lockdown also a drag on sentiment.

The UK’s FTSE 100 is the laggard now, down 98 points or 1.5%, with the wider Stoxx 600 now off 0.6%.

European stock markets, July 07 2020 Photograph: Refinitiv

Connor Campbell of Spreadex says the Summer Forecasts poured some unseasonal cold water on the markets:

Already fearful of the covid-19 situation in the US and Australia – Melbourne has just been put in a 6-week lockdown – the European Commission’s latest forecasts merely compounded the market’s concerns on Tuesday.

The broad direction of the bloc’s GDP revisions was sharply downwards. As a whole the European Union is now facing am 8.3% contraction in 2020, compared to the 7.4% estimate announced in May. France saw one of the more significant changes, the country looking at a 10.6% drop, far higher than the 8.2% decline initial forecast.

Spain and Italy were both dealt their own ugly numbers, heading for -11.2% and -10.9% respectively. Germany, on the other hand, saw a minor improvement, their typical Teutonic efficiency resulting in a move from -6.5% to -6.3%.

Just in: the number of job vacancies in the US has risen, as companies emerged from their Covid-19 lockdowns.

Job openings rose to 5.397m in May, the US Labor Department reports, up from 4.996m in April. New hires jumped to, from 4m to 6.68m.

That backs up the message from recent Non-Farm Payroll reports, that US companies took on more staff in May and June.

It’s an encouraging sign, but economists are pointing out that the labor market is still weak:

Daniel Zhao (@DanielBZhao)

May #JOLTS report from BLS:

Job openings at end of May rebounded to 5.4 million, up 8% MoM, but still down 26% YoY

Puts us back at 2015 levels for job openings and consistent w/ recovery in May #JobsReport

Latest #JOLTS data out now! In May, the number of hires increased by 2.4 million to a series high of 6.5 million, the largest monthly increase and largest number of hires on record (series began in 2000). I still expect considerable weakness this summer.t.co/SCkgCKTPHN

July 7, 2020

Heidi Shierholz (@hshierholz)

Both surveys show we remain in an enormous jobs deficit given the jobs lost in March and April. We were down 13.1 million jobs at the end of May (according to the JOLTS data), and down 14.7 million at the middle of June (according to the monthly employment data). 6/

July 7, 2020

Jennifer Jacobs (@JenniferJJacobs)

U.S. stocks end a 5-day rally, the longest since December, as investors face the possibility of a longer-than-expected economic recovery amid coronavirus, @business reports.

Nine of 11 S&P 500 sectors declined. Dow Jones Industrial Average down.

July 7, 2020

The New York Stock Exchange on Wall Street Photograph: Angela Weiss/AFP/Getty Images

Over in New York, stocks have opened lower after five days of gains.

The Dow Jones industrial average has dropped by 226 points, or almost 0.9%, to 26,060. Last night, it closed at a three-week high.

The S&P 500 is down 0.4% while the Nasdaq, which hit a new record high last night, is flat.

Economic optimism had lifted stocks sharply in recent days. But the new lockdown in Melbourne is a reminder of the risks of a second wave of Covid-19 infections — as global infections continue to rise sharply.

David Riley, chief investment strategist at BlueBay Asset Management, says some investors are too optimistic about the economic recovery (unlike the EC today!)

“Investors are in danger of extrapolating a bounce in the economy from the unprecedented declines in activity in the second quarter into a rapid and complete V-shaped recovery. It is simply too early to make a definitive judgement on the shape of the economic recovery, but it is optimistic to believe that the pandemic will not have deep and lingering effects on consumers and businesses even as the virus is brought under control.

“Countries that were more successful in containing the virus will recover more quickly than those that were not. China and other countries in the region that have largely eliminated the virus are benefiting from a more sustained economic rebound as business open-up and consumers are more confident to venture out and spend, supporting jobs and growth.

In many ‘Western’ countries, economies are re-opening with higher infection rates and greater risk of renewed outbreaks that erode business and consumer confidence and weaken the economic recovery.

I’m always a sucker for brightly-coloured charts, and this one shows nicely how the US stock market had clawed its way back from its slump in February and March:

Michael McDonough (@M_McDonough)

Annual performance of the S&P 500 over the past 29 years — white line is 2020 ytd: pic.twitter.com/mrrtt1Dv2v

July 7, 2020

A customer is greeted by an employee at the entrance to a Shake Shack restaurant, last month. Photograph: Steven Senne/AP

US fast food restaurant chain Shake Shack has reported a hefty slump in sales during the Covid-19 pandemic

In its latest financial results, the seller of burgers, hot dogs and frozen custard (I kid you not) reports that it has reopened many outlets. However, sales were still down over 40% in the five weeks to June 24th.

Takings are picking up, but are particularly slow in New York, a key sales region.

It tells shareholders:

Same-Shack sales for the most recent week ended July 1 were down (39%), with the overall speed of company-wide sales recovery remaining uncertain due to ongoing volatility related to COVID-19.

In addition, same-Shack sales remain acutely impacted by New York City, one of the Company’s largest regions with some of the highest volume Shacks, which is expected to take a longer period of time to fully recover than other parts of the country.

For the most recent fiscal week ended July 1, New York City same-Shack sales were down (58%) versus the prior year, and with this region accounting for approximately 20% of the Company’s total Shack sales in the first quarter prior to the COVID-19 outbreak, it will continue to have a notable impact on total Company sales performance until there is a material recovery.

UK technology firm Micro Focus are the top faller in London today after posting a $1bn loss for the last half-year, and warning that conditions are unlikely to improve.

Micro Focus, one of the UK’s biggest tech companies, blamed the Covid-19 pandemic as it took a $922m impairment charge due to heightened economic uncertainty.

The firm bought Hewlett-Packard’s software business in 2017 for nearly £9bn, but has suffered “disruption to new sales activity and timing pressure on renewals” since the lockdown started.

Customers have been putting off renewing their software licences while they work out their future needs, now that many staff are working from home.

This situation may not improve for some time, with the company telling shareholders that:

Despite the resilience of Micro Focus’ customer proposition and financial model, the ultimate impact on the global economy of the COVID-19 pandemic remains unclear, as does the timing and extent to which that impact flows through into customer spending plans on enterprise software.

Our current assumption is macro-economic conditions are unlikely to improve in the second half of the financial year.

As a minimum, we continue to believe it appropriate to be prepared for further disruption to our new sales activity and timing pressure on renewals.

Shares in Micro Focus are down 14.5%, at the bottom of the FTSE 250 index. They’ve now lost two-thirds of their value this year.

People queue outside the River Island store on London’s Oxford Street after the shops were allowed to reopen. Photograph: Dave Rushen/SOPA Images/REX/Shutterstock

Fashion chain River Island has joined the swelling ranks of retailers cutting staff.

Retail Week reports that 250 head office jobs are being cut. This follows a slump in sales since the pandemic began, even though stores did reopen last month.

They explain:

In an internal email sent to staff seen by Retail Week, River Island boss Will Kernan said the business will “now have a requirement for some 250 fewer people in the business”.

Retail Week understands these redundancies will be made across all the retailer’s head office departments.

More gloom: the OECD has warned that UK unemployment is on track to hit its highest level in decades, especially if we suffer another surge in Covid-19 cases.

My colleague Phillip Inman explains:

The number of unemployed people in Britain could soar to almost 15% of the working population if the country experiences a second wave of the coronavirus pandemic, the Organisation for Economic Cooperation and Development (OECD) has said.

A rise in the unemployment rate to 14.8% would take the UK to a higher level than France, Germany and Italy, but lower than Spain, according to the Paris-based thinktank, which is funded by 35 mostly rich countries.

If a second wave of Covid-19 can be avoided, the UK’s unemployment rate is likely to rise to 11.7% by the end of the year, the highest level since 1984 when it peaked at 11.9%. The current UK unemployment rate is 3.9%.