US economy added 1.8m jobs in July, beating expectations – as it happened

The US economy is rebounding, but at a slower rate than before – suggesting the economic damage caused by the pandemic and the lockdowns will be protracted.

The US economy added 1.8m jobs in July, more than expected but still a long way short of the previous month’s 4.8m jobs gain – perhaps unsurprising given further outbreaks and tighter restrictions.

Chris Williamson

(@WilliamsonChris)The US was the only major economy to see COVID-19 containment measures TIGHTEN on average in July pic.twitter.com/Cb8msDyw60

August 7, 2020

That meant unemployment at 10.2%, again better than expected, but still at a level unprecedented since before the second world war.

There is likely to be a similar story in the UK, where the withdrawal of the government’s furlough scheme is likely to lead to a renewed jump in unemployment as we move towards winter, and the end of the job retention scheme on 31 October.

Chancellor Rishi Sunak today said he did not want workers to be “trapped” in furlough, suggesting he is unlikely to give in to opposition demands to extend the scheme to parts of the economy that are still unable to open.

Here are some of the other important developments from today:

- The Evening Standard newspaper, which serves London’s commuters, is to cut a third of its staff after a dramatic reduction in revenues during the pandemic.

- UK house prices took economists by surprise with a “mini-boom”, up 1.6% in July according to Halifax. It is not expected to last, however.

- The UK government has announced a £355m package to cushion Northern Ireland businesses from the costs of trading with the rest of the UK because of Brexit.

- More than 6,000 British Airways staff have accepted voluntary redundancy as the airline moves to tell thousands more cabin crew and ground staff whether or not they will keep their jobs or face pay cuts.

- TikTok threatened legal action in the US after an executive order issued by President Donald Trump said US companies have 45 days to stop all transactions with TikTok’s owner, ByteDance, as well as Tencent, the Chinese owner of WeChat.

You can continue to follow our live coverage of the coronavirus outbreak around the world:

In the UK, coronavirus’s community spread in England may be levelling off, says the Office for National Statistics

In the US, the death toll tops 160,000 as relief package impasse continues

In our global coverage, Norway advises citizens to avoid all travel abroad; PPE destroyed in Beirut blast

Thank you as ever for following our live coverage of business, economics and financial markets. Please do join us on Monday for more. JJ

Sterling is now down by 0.7% against the US dollar in the wake of the jobs numbers.

One pound will buy $1.3061, down from $1.314 early this morning – although there has been some volatility (as ever) as traders digested the non-farm payrolls data.

The euro fell by 0.7% against the dollar, to $1.1799.

The unemployment rate has now fallen for three months in a row, but it remains above the 10% peak of the Great Recession and is three times the 3.5% rate from February, before the spread of the pandemic in the US.

July’s jobs increase was less than the 4.8m jobs added in June and 2.7m added in May.

The largest gains were in leisure and hospitality, which increased by 592,000 as coronavirus restrictions were lifted. Employment in food services and drinking places rose by 502,000. Despite the gains over the last three months, employment in food services and drinking places is down by 2.6m since February.

Read the full report here:

More reactions from economists and commentators who are suggesting the headline figures don’t quite tell the full story:

John Philpott

(@JobsEconomist)More like a sign of continued improvement than a ‘bounce back’. Would nonetheless be encouraging were it not for the fact that #COVID__19 is still far from under control in many parts of the United States. t.co/vBBvs9X6Sw

August 7, 2020

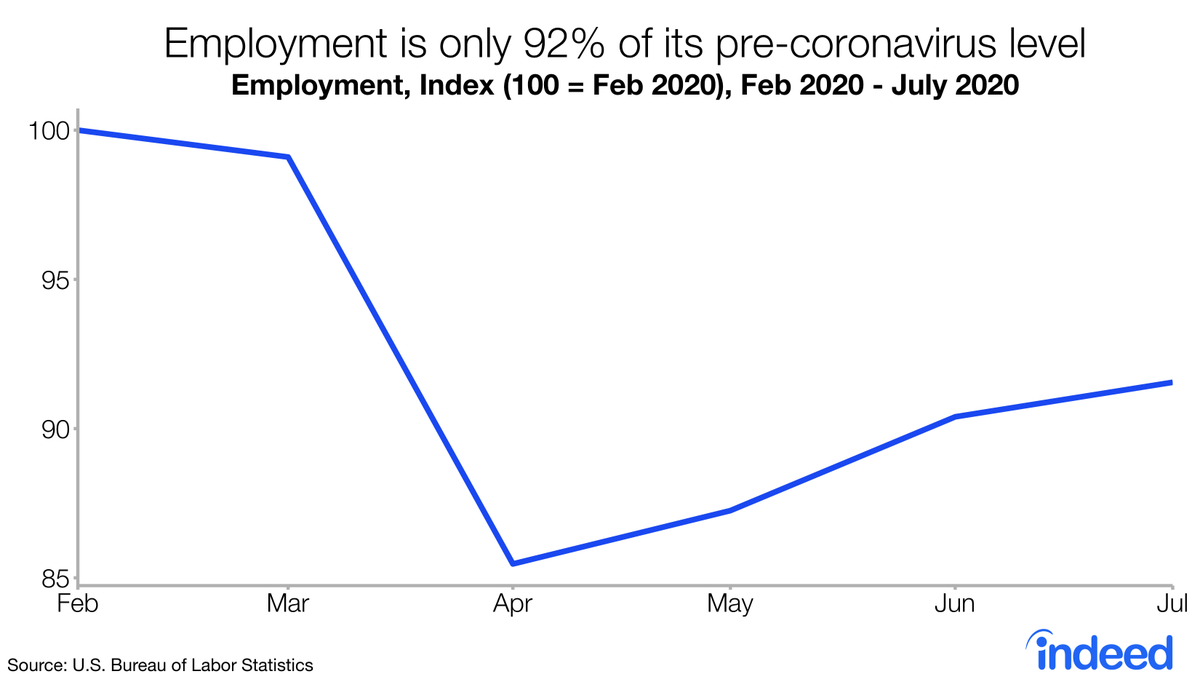

Nick Bunker

(@nick_bunker)Employment is still 8% below its February level. 1.8 million jobs isn’t V-shaped recovery speed. pic.twitter.com/bLYdATAkHa

August 7, 2020

Heather Long

(@byHeatherLong)This recession continues to hit Black and Hispanic workers the hardest.

July unemployment rate for…

White men: 8.3%

White women: 9.6%

Black men: 15.2%

Black women: 13.5%

Hispanic men: 11.4%

Hispanic women: 14.0%(Note these rates are for workers over age 20)

August 7, 2020

This chart shows just how bad it is for the US economy, despite the big jobs rebound. If the red line is anything other than a “V” it means a protracted period of gloom.

Bill McBride

(@calculatedrisk)July Employment Report: 1.8 Million Jobs Added, 10.2% Unemployment Rate t.co/LeKFERKlo8 pic.twitter.com/BQ3DoWIgma

August 7, 2020

Read the original article at The Guardian